Navigating the British Healthcare Maze: A Definitive Guide to Expat Health Insurance in the UK

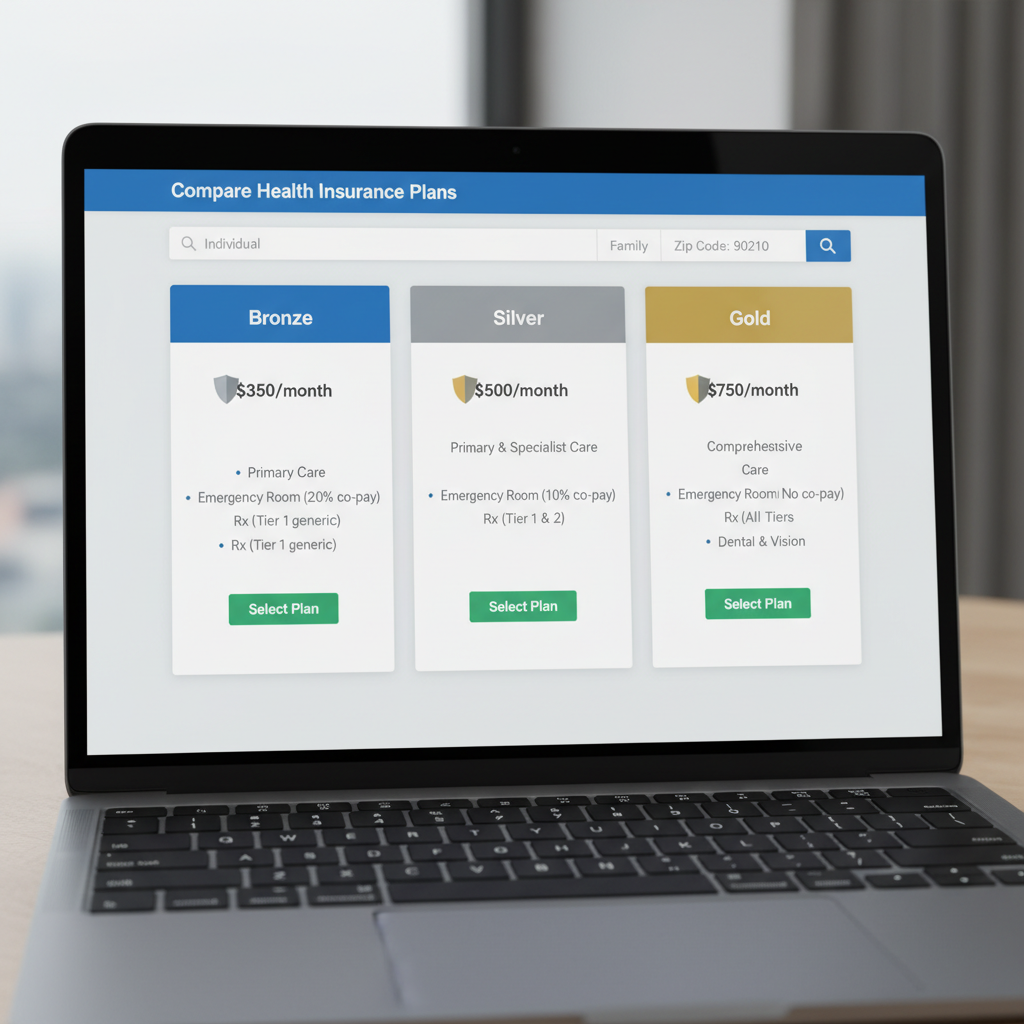

Moving to the United Kingdom is a dream for many, offering a blend of historic charm, economic opportunity, and a vibrant multicultural landscape. However, one of the most critical hurdles for any expatriate is understanding how to protect their health in a system that is often lauded but increasingly strained. While the National Health Service (NHS) remains the backbone of British life, the reality for modern expats is that relying solely on public care may not align with their expectations for speed and convenience. Choosing the right expat health insurance is no longer just a luxury; it has become a strategic necessity for those who value their time and peace of mind. [IMAGEPROMPT: A professional expat sitting in a bright London cafe, reviewing health insurance documents on a tablet with the Shard visible in the background.] ## The Paradox of the NHS and the Immigration Health Surcharge. For most expats, their first encounter with the UK healthcare system is the Immigration Health Surcharge (IHS). This mandatory fee, paid during the visa application process, grants access to the NHS on a similar basis to permanent residents. It covers everything from GP consultations to emergency room visits. However, paying the surcharge does not mean you have escaped the long waiting lists that currently plague the system. As of 2024, the NHS faces historic backlogs for elective surgeries and specialist consultations, making the public route a frustrating experience for those needing non-urgent care. Private health insurance serves as a crucial bridge over these systemic gaps. By opting for a private policy, expats can bypass the 18-week (or longer) waiting targets for specialist diagnostics and treatments. This is particularly vital for professionals who cannot afford weeks of downtime or uncertainty regarding their health. It is not about replacing the NHS, but rather supplementing it with a layer of efficiency that the public sector currently struggles to provide. ## Local Private Health Insurance vs. International Plans. When exploring insurance options, expats generally face two choices: Local Private Medical Insurance (PMI) or International Private Medical Insurance (IPMI). Local PMI is designed specifically for the UK market. These plans are often more affordable and focus on providing access to private hospitals like those run by Bupa, Nuffield Health, or Ramsay. They are ideal for expats who plan to stay in the UK long-term and do not travel frequently for work or leisure. [IMAGEPROMPT: A sleek, modern private hospital corridor in London with high-end medical equipment and professional staff in the distance.] On the other hand, IPMI plans are built for the global nomad. These policies are much more robust, offering coverage across multiple countries and often including ‘out-of-area’ benefits. If your career requires you to move between London, New York, and Dubai, an international plan ensures continuity of care without the need to switch providers every time you cross a border. While the premiums for IPMI are significantly higher, the flexibility and higher coverage limits for chronic conditions often justify the cost for high-net-worth individuals and corporate executives. ## Essential Coverage Components for Expats. Not all health insurance policies are created equal, and for an expat, certain features are non-negotiable. At the very least, a policy should cover inpatient and day-patient care, which includes hospital stays and surgeries. However, the true value of a policy often lies in its ‘outpatient’ coverage. This includes consultations with specialists, diagnostic tests like MRIs and CT scans, and physiotherapy. Without outpatient cover, you might find yourself waiting months for an NHS specialist just to get a diagnosis, even if your insurance is ready to pay for the eventual surgery. Furthermore, mental health support has become a priority in modern insurance packages. The transition to a new country can be taxing, and many UK insurers now offer robust mental health pathways, including remote counseling and psychiatric support. Other optional add-ons to consider include: Full Cancer Cover: Providing access to experimental drugs and treatments not always available on the NHS. Dental and Optical: While often restricted, these are useful for routine maintenance. * Virtual GP Services: Allowing 24/7 access to a doctor via video call, bypassing the local GP booking system. ## Decoding Premiums and the ‘Moratorium’ Mystery. Understanding the cost of your insurance requires a look at how UK insurers assess risk. Your age, lifestyle, and the specific hospital list you choose (London-based hospitals are significantly more expensive) will dictate your premium. However, the most confusing aspect for newcomers is the ‘underwriting’ process. Most UK insurers use ‘Moratorium’ underwriting, which means they will not cover any medical condition you have had in the last five years until you have been symptom-free for a continuous period (usually two years) after the policy starts.

Alternatively, ‘Full Medical Underwriting’ requires you to disclose your entire medical history upfront. While this involves more paperwork, it provides absolute clarity on what is and isn’t covered from day one. For expats with pre-existing conditions, navigating these terms with a specialist broker is highly recommended to avoid claim rejections during a medical crisis. Ultimately, the best expat health insurance in the UK is one that offers a balance between comprehensive clinical access and financial sustainability. By understanding the interplay between the NHS and private providers, you can ensure that your time in the UK is defined by your experiences, not by the time you spend in a waiting room.